Beauty Contests

Morningstar, The Fiduciary Rule, and the Unreasonable Tyranny of “Prudence”

Recently, BlackRock launched the iShares Top 20 U.S. Stocks ETF ( TOPT 0.00%↑ ). The day the fund began trading, my subway car into Manhattan was plastered with ads for the fund. “20 BIG STOCKS, 1 SIMPLE TRADE,” the copy read on nearly every imaginable surface. I have no idea if this kind of well-timed ad spend is a positive ROI for BlackRock, but I’m more interested in what it is trying to convey.

Brevity and compliance restrictions prevent BlackRock from elucidating why you might want to own just the Top 20 companies by free-float adjusted market capitalization or why you should pay 20 basis points for the pleasure of having them do it for you. Ease is one clear message, but more so is the preponderance of BlackRock, with its $10 trillion of assets under management, as the investment manager de rigueur for the transit class. They made it, and now you’ll buy it.

There are two important channels of communication in financial markets. One is between companies, governments, various securities issuers, and asset managers. The other is between asset managers and the savers whose funds they invest. How do the mediators of capital— the wealth advisors, pensions, and foundations, pick the relative winners in the great asset-gathering game?

Regulation, litigation, and competition sparked a devolution of investment management. The industry has taken on beauty pageant-like dynamics, where once subjective judiciousness aimed at identifying the exceptional has been reduced to a strict rubric that produces homogenous, uninspiring investment options. A crowded stage of wax figures all calling for world peace.

Style Boxes & Stars

In an earlier era, actively managed mutual funds were once the predominant investment vehicle. Before the rise of passive investing (to be addressed shortly), capital allocation aimed to identify superior investment managers. In 1985, a then-small Chicago-based company called Morningstar introduced a simple innovation: a five-star rating system for mutual funds. Seven years later, they launched an even more influential tool: the Style Box. Together, these two innovations would fundamentally transform how Americans invest their money.

Before Morningstar, investing in mutual funds was like navigating without a map. Every fund company used different terms to describe their strategies, making comparisons nearly impossible. The Style Box changed this overnight by introducing a nine-square grid that classified funds based on two simple factors: market capitalization (small to large) and investment style (value to growth).

The Star Rating system was equally revolutionary. By distributing ratings on a bell curve within each category (10% getting five stars, 22.5% four stars, 35% three stars, and so on), Morningstar created a universal language for fund evaluation. Though controversial for its backward-looking nature, the system's influence was undeniable—a single ratings change could move billions of dollars.

Asset management is a cascade of principal-agent problems. Most investment managers want to grow and retain the assets on which they charge fees. That means not getting fired by your clients. The easiest way to get fired is by looking too different from the competition and being wrong. The result is a lot of active managers who look very close to their respective benchmarks. This approach generates uninspiring investment returns but creates a more stable business for asset managers.

Box Jumping

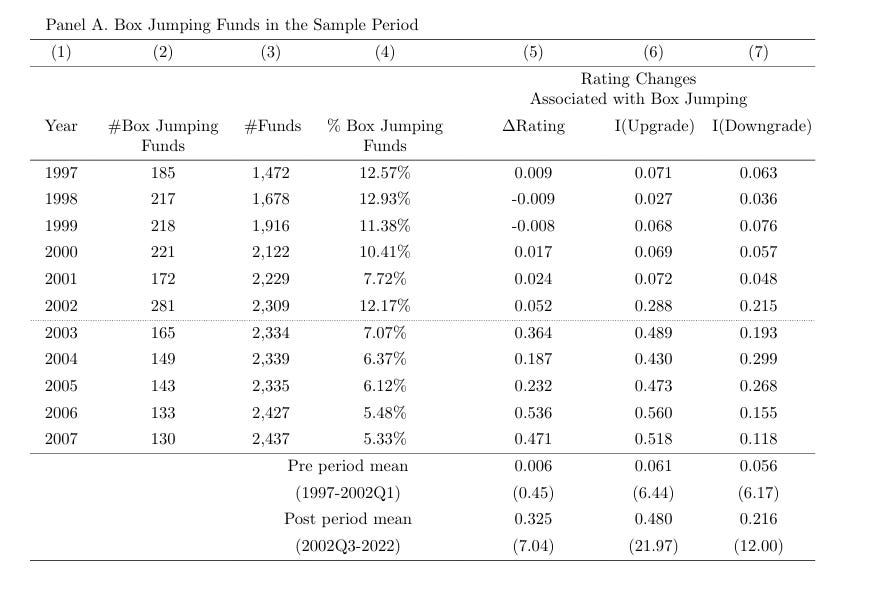

The Star Rating system gave managers a reason to take more active risk; outperforming their peers could lead to massive inflows. Of course, Goodhart’s Law, “When a measure becomes a target, it ceases to be a good measure,” took hold. A new paper, “Box Jumping: Portfolio Recompositions to Achieve Higher Morningstar Ratings” by researchers at Harvard Business School and MIT Sloan explains “mutual fund managers strategically alter their portfolios to take advantage of investors’ reliance on Morningstar star ratings.”

In 2002, Morningstar made what seemed like a logical improvement to its mutual fund rating system. Instead of comparing all equity funds against each other, they decided to compare funds only against their peers with similar investment styles. On the surface, this made perfect sense – after all, why compare a conservative large-cap value fund against an aggressive small-cap growth fund?

The new system created nine distinct categories based on market capitalization (large, mid, and small) and investment style (value, blend, and growth). Within each category, funds would be ranked against each other. This meant a fund would only be compared against others pursuing similar investment strategies. When a fund moved from one category to another – say, from large-growth to large-blend – Morningstar would immediately start comparing its historical performance against funds in the new category.

“To illustrate our approach, consider the case of Goldman Sachs U.S. Equity ESG A (ticker: GAGVX). This fund was categorized as a Large Growth fund from December 2012 until May 2021, when it box jumped to the Large Blend category …. Despite a slight decline in its three-year trailing returns– from 14.5% in April 2021 to 14.2% in May 2021– the fund’s three-year Morningstar rating increased from three stars to five stars due to its new comparison group, which had worse historical returns. Following the rating upgrade, the fund experienced significant benefits. Notably, it shifted from experiencing outflows to inflows, receiving approximately 1% of inflow per month in the six months after the box jump, compared to monthly outflows of-0.4% in the preceding six months. Additionally, the fund raised its management fee by 150 basis points after the jump.”

Overall, the researchers found that about 9% of Funds box jump annually. Those funds are twice as likely to receive an upgrade than a downgrade when box jumping. The rewards were substantial: successful box jumpers saw their assets under management increase by 6.7% on average and were able to charge 5% higher fees on average.

Before 2002, only 6% of funds that changed categories received rating upgrades. After the change, that number jumped to 48%. But there was a catch. The portfolio changes required to qualify for a new category often led to worse investment performance. Funds that engaged in box jumping typically saw their returns fall by about 21 basis points per quarter. Even more tellingly, the rating upgrades achieved through box jumping usually reversed within three years.

The statistical tools used to evaluate manager performance are a kind of financial phrenology that uses the shape of the past to make decisions about the future. Sharpe ratios, information coefficients, Sortino ratios, and Traynor ratios all describe how a manager’s returns relate to a benchmark, but there is no reason to believe that any manager can pursue high-risk-adjusted returns within the confines of these measures.

The identity of risk and reward nearly ensures that great performance will come at the expense of the risk measures at some point in time. The capital allocator seeks a consistent framework to make, in the wisdom of institutions, prudent decisions. Morningstar provided such a framework.

Style Boxes & Star Ratings became an essential channel of communication between asset managers and savers. Were capital allocators such easy marks that a relatively rudimental stamp of approval substituted the kind of analysis their professions claimed to practice? In part, yes, the capital allocators have bosses of their own, and like the asset managers they invested with, they too, prefer to remain employed. There is career risk in allocating to poorly rated funds.

But that was only the beginning of the “outsourced thinking” to come. Prudence itself was about to get a legal definition.

The Fiduciary Rule

The Department of Labor's 2016 Fiduciary Rule marked a crucial turning point by elevating the standards for investment advice in retirement accounts. The rule required advisors to document and justify their investment recommendations, emphasizing fee reasonableness. This regulatory change coincided with the existing influence of Morningstar's evaluation framework.