Winning with the Losers

Dolby Laboratories, AI Losers, and the usefulness of a stock that just won't go up

The global consultancy Accenture ACN 0.00%↑, and its 780,000 employees, finds its stock price halved in the first six months of this year. As though added to some dishonorable registry, Accenture is now an “AI Loser.” The label will be hard to shake.

Founding members of the club like Chegg CHGG 0.00%↑ and Upwork UPWK 0.00%↑democratized developing-market labor arbitrage. Those companies have lost more than 90% of their market capitalization since the release of ChatGPT.

In 2020, I was thrilled to pay $30 for someone in the eastern hemisphere to transpose data from a 30 page offering memorandum into Excel overnight. The obvious obsolescence of that model with the state of LLMs and its relevance to Accenture are matters of degree not type.

Profiting off of these disruptions on the short side would have required a unique disposition. One would have had to have foreseen the growing distribution and power of AI, and sought out capped-upside shorts instead of the “picks and shovels” longs that have pulled years of prospective cash flow into their share prices in a matter of months. That’s neither intuitive nor particularly prudent if a paradigm shift is indeed underway.

I have written before about my ambivalence towards the boldest predictions about the impact of AI, but the technology is no doubt upending the business models of many companies in ways that are not as obvious as they were for Chegg and Upwork.

There is a compelling opportunity to short companies for whom AI presents merely a secular headwind, not an existential risk. Dolby Laboratories DLB 0.00%↑ is one such example.

Using shorts strategically

Before I get into Dolby, I want to lay out a framework for short-selling that serves a longer-term purpose than is typically associated with the practice. Short-sellers, particularly ones who make it part of their identity, face an uphill battle.

The most they can make on any short is 100%. Identifying frauds, while noble, does not guarantee profits. In fact, a fraudulent company is actually at a distinct advantage. Once a management team has sloughed off any ethical shackles it can undertake a number of strategies to drive the stock price higher in the near term.

Timing the inevitable collapse becomes near impossible without engaging in the rabble-rousing that sullies the reputation of short-sellers with charges of market manipulation. There is rarely an apology tour when and if they are ultimately proved right.

Two realities led me to shorting as a strategic tool in portfolio management. First, the market is very hard to beat. Since mid-century, data has shown that active management rarely beats the index. At the same time, an analysis of individual stock returns reveals that most stocks go down. This means that the proverbial “monkeys throwing darts” might conceivably be decent short-sellers.

Therefore, those looking to beat the market can be well-served by simply owning the market and selectively shorting stocks facing secular headwinds. The odds are actually in your favor for doing this successfully.

Of course, shorting carries distinct risks. The asymmetry of outcomes means the isolated of expected value of a single short is almost always negative. Secondly, highly shorted companies face the possibility of mechanical buying in a squeeze. Finally, over the long-run it makes sense to not just be net long the market, but optimally to deploy a degree of leverage can enhance returns. Even profitable shorting reduces your net market exposure.

What you really want in a short-candidate is not a stock that will necessarily have a precipitous drop, but rather one that faces overwhelming headwinds for going up. Such stocks effectively provide cheap leverage for funding levered exposure either to the market or to overweight fundamental longs.

Unlike identifying frauds or shorting fantastical valuations, both of which involve a high degree of timing risks, finding stocks with secular constraints on both their business and multiple is relatively easier. Further, these shorts need not be tactical. Since they are rarely the target of classic short-sellers the borrow rate is typically cheap and the risks of a short-squeeze nearly eliminated. Again, you just want to find to a stock that is unlikely to go up.

In general these companies typically demonstrate one or all of the following characteristics:

A business model that serves a declining industry or one with a shrinking TAM.

Family control or other governance blockers that reduce the likelihood of buyout or M&A.

Inflated multiple from inclusion in thematic ETFs or other passive vehicles that support share price in absence of natural buyers.

Low short-interest

Minimal return of shareholder capital

Dolby Laboratories Inc.

Most people are familiar with the Dolby brand, either from the movie theater, a small decal on their flatscreen TV, or from their car stereo system. What most people don’t realize is that Dolby doesn’t manufacture anything. No speaker wire is coiled, no cathodes, grids or plates are assembled into amplifiers, Dolby doesn’t design components or finished goods at all. Dolby is a royalty company. It licenses its brand and technology related to the digital compression of audio and video content.

In many cases, Dolby has only invented a portion of the process used for compression and the licensing revenue it collects is from a syndicate of patent holders that contribute to the finished technology. Aside from its internally generated IP, the company will also acquire patents to hold in its portfolio, recently purchasing a portfolio of patents from GE. More on that shortly.

As primarily a licensor, Dolby has fantastic margins. For fiscal 2025, which ended in September, the company generated $379 million of EBITDA on $1.35 billion in sales. This business has ~90% gross margins and near 30% EBITDA margins. When you purchase a flat-screen TV, that manufacturer has to pay a unit-based margin to Dolby for the technology that reads compressed audio and video content and presents it on the screen. These technologies are called codecs and for much of the last 30 years Dolby has benefited from holding onto the patents on the standard-bearing versions as the price of consumer electronics fell and their end markets grew.

These patents are expiring. The company does not disclose the exact expiration schedule but much of the audio codec portfolio is set to expire in the next five years. Moreover, the licensing is at the unit level, so Dolby has no exposure to the rapid growth of streaming or the general expansion of “screen time.” These are not usage based licenses, the technology gets embedded in the TV, car stereo system or smartphone.

Dolby is working on usage based licensing for things like live sports, but the segment is small and the use cases are less ubiquitous than simply translating all compressed audio or visual content.

A brief exploration of AI impacts on codec technologies

Audio, as you may remember from science or physics class, is a collection of sound waves. Each sound wave has essentially an infinite number of vectors. As a result a raw audio file is enormous from a data storage and transmission perspective. What compression does is convert that wave data into something more like a bar chart.

The width of the bars is roughly translatable to the level of compression. More skinny bars is less compression, while wider, less frequent bars mean more compression. The difference between the audio you hear from legacy physical media like a compact disc to what gets delivered over Spotify is roughly 4:1.

This is required for all transmission of content over normal broadband data speeds. Video compression is even more complex and the technology relies on effectively making educated guesses from reference pixels. A frame of video with blue sky in the background might only pass a subset of pixels for each frame and then the technology says “Ok, this pixel is blue, the one next to it is probably also blue.”

You can probably already surmise the impact that the increasing power of AI could have on Dolby’s core business. Disclosed risk factors are usually comprehensive to the point of meaninglessness, but Dolby only began including the following in their risk disclosures in 2023:

“Competitors may also be able to develop and market new technologies that render our existing or future products less competitive. For example, advances in AI/ML may enable competitors to develop competing technologies more rapidly and with fewer resources, or to develop products that incorporate AI/ML in a way that makes them more effective, than has historically been possible. Such use of disruptive technologies could significantly alter the market for our products in unpredictable ways.”

All AI disruptions are still firmly in the realm of speculation but the impact on Dolby is more grounded in what technology actually does. AI generated content does not require such compression. In a more fantastical future you may be able to assemble, say, an episode of Fargo on the fly versus transmitting compressed content. That still faces some hard technological limitations that don’t entirely remove the data transmission but does render traditional codecs less valuable.

Dolby has been through multiple restructurings to try to adapt their cost structure to this reality, but the company still has more than 2,000 employees. As of March 2026, SG&A is 67% of revenues. Dolby spends around $250 million per year on research and development. Suffice to say that spending is not gone towards forging a Dolby brand at the vanguard of AI technologies.

Family control

Ray Dolby cut an envyable path as an entrepreneur. He founded Dolby in London in 1965 with a staff of just four people. In that same year he invented and patented his noise-reduction technology. Crucially, he bootstrapped it on product revenue rather than investor capital. The first product, the A301 professional noise-reduction unit, was sold to Decca Records for about £700 in 1966, and the business was built from licensing and equipment sales from there. The company grew on operating cash flows for R&D and expansion rather than venture capital, with concentrated equity held in the Dolby family and with limited outside dilution.

Heading into Dolby’s 2005 IPO, Ray Dolby held 98.2% of the Class B common stock concentrated in the founder and family trusts, with no meaningful roster of venture investors, private-equity backers, or strategic minority holders to speak of. The only "outside" equity of any consequence was incentive stock granted to employees over time — and even that was modest relative to the founder's stake.

Today, Dolby is a public company that functions, for control purposes, as a private family holding. Its dual-class structure carried over from the 2005 IPO gives publicly traded Class A shares carry one vote each, while the Class B shares held by the Dolby family carry ten.

That ratio gives the family around 85% of total voting power while holding a much smaller share of the economics. There is no sunset provision that would eventually collapse the two classes into one, and the family keeps effective control even as its economic stake declines, because Class B only converts to Class A on transfer outside a defined set of permitted family transferees. Ordinary succession within the family therefore doesn't erode the voting lock.

Last year the Dolby family collected almost $50 million in dividends on the company’s $255 million in earnings and $126 million of total dividends. I flag this to point out how challenging it would be for Dolby to be acquired. Annuitizing the Dolby family’s dividend alone would cost nearly one quarter of the market capitalization before accounting for any control premium.

Additionally, because of how Dolby’s royalties are structured and accounted for, the company carries no debt. When Dolby enters a contract it books the expected value of that contract to revenue, and creates a balance sheet entry for the contract value. As actual unit sales are realized the company either debits or credits revenue and adjusts the balance sheet account.

Those revenue projections are based on modeling from a third party. Dolby’s auditors have flagged this practice in their opinion letters saying effectively that that it has historically been an accurate representation of economic reality, but that there is no guarantee that it will continue to be.

The result is that Dolby is levered to cyclicals (consumer electronics, auto) but really only has downside exposure from the way they book contract revenue. In an up-cycle they book revenue immediately, when the cycle turns that revenue gets reduced as actual unit sales materialize slower.

This is all to say that there are few levers for either management or shareholders to pull to generate greater equity returns. Shareholders will be likely be unsuccessful in pushing for a buyout, similarly management is constrained from financially engineering higher returns through the use of debt.

In fact, the company’s only option is to continue to invest cash flow into R&D which limits how much operating margins can be expanded. Purchasing patents, like the GE deal, is becoming more like maintenance CapEx as patents expire.

Valuations, or, why bother?

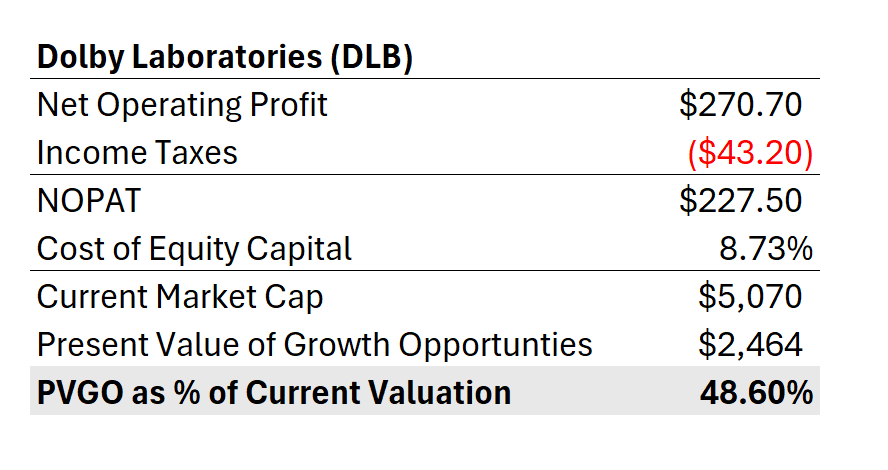

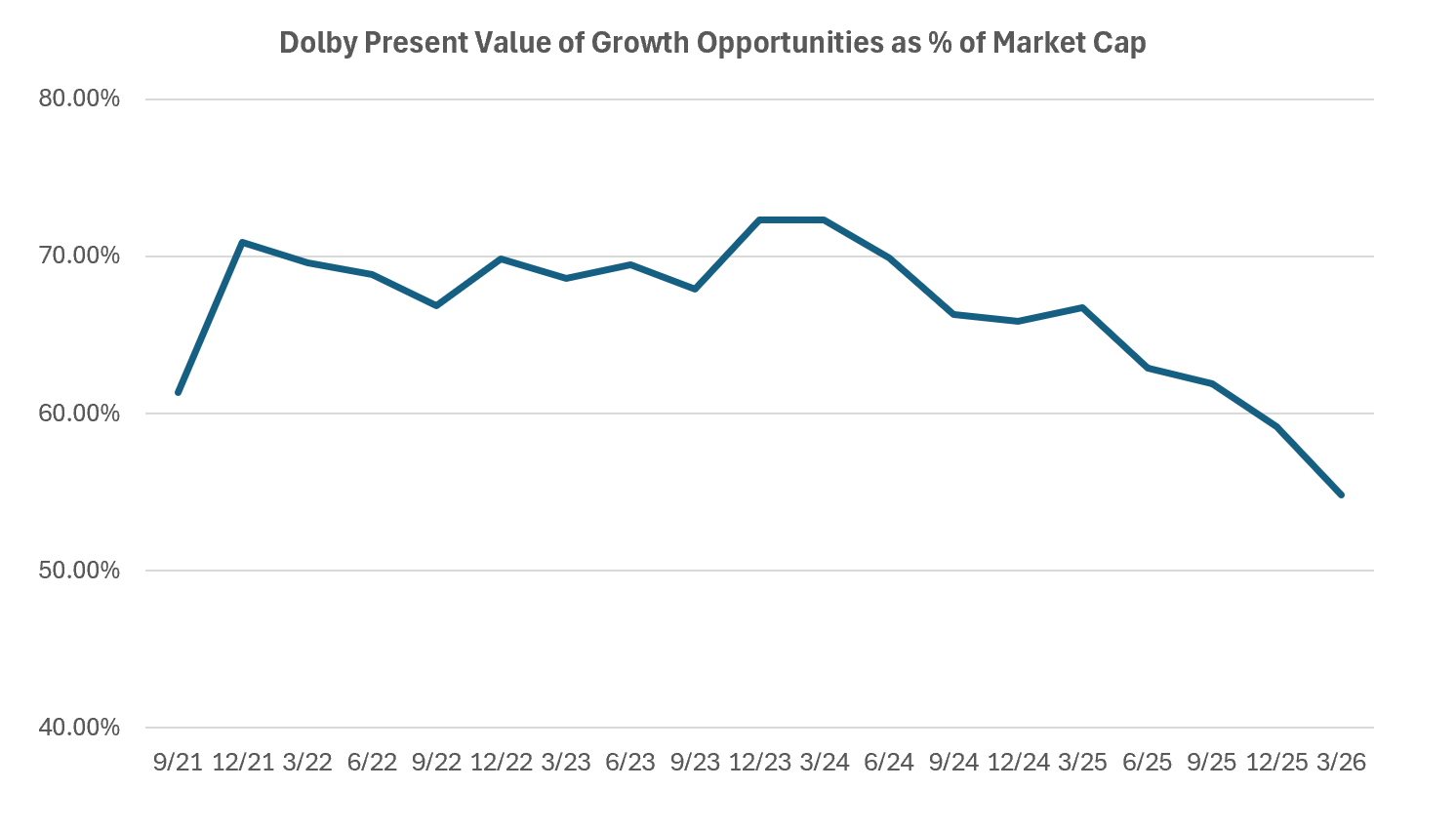

Dolby’s multiple has fallen even as EPS estimates and guides have increased. Dolby’s LTM NOPAT (Net Operating Profit after Tax) is $270 million. Using Mauboussin’s Present Value of Growth Opportunities calculation, close to half of the stock’s value is still embedded in future growth expectations.

High-flying companies like NVDA 0.00%↑ have closer to 80% of their value in PVGO, so Dolby’s <50% number looks “cheap” in some respects, but the trend is lower.

Increasingly, Dolby’s valuation is captured in the present value of its steady-state earnings power, which, as covered above, is under a variety of attacks.

Recall, Dolby’s purchase of the GE patent portfolio. Management presents this as growth Capex, but in reality, it is required to offset the very real depreciation of the patents. This creates an accounting artifact that makes Dolby’s business look stronger than it actually is. The purchase will be amortized, and that amortization will be added back to free cash flow.

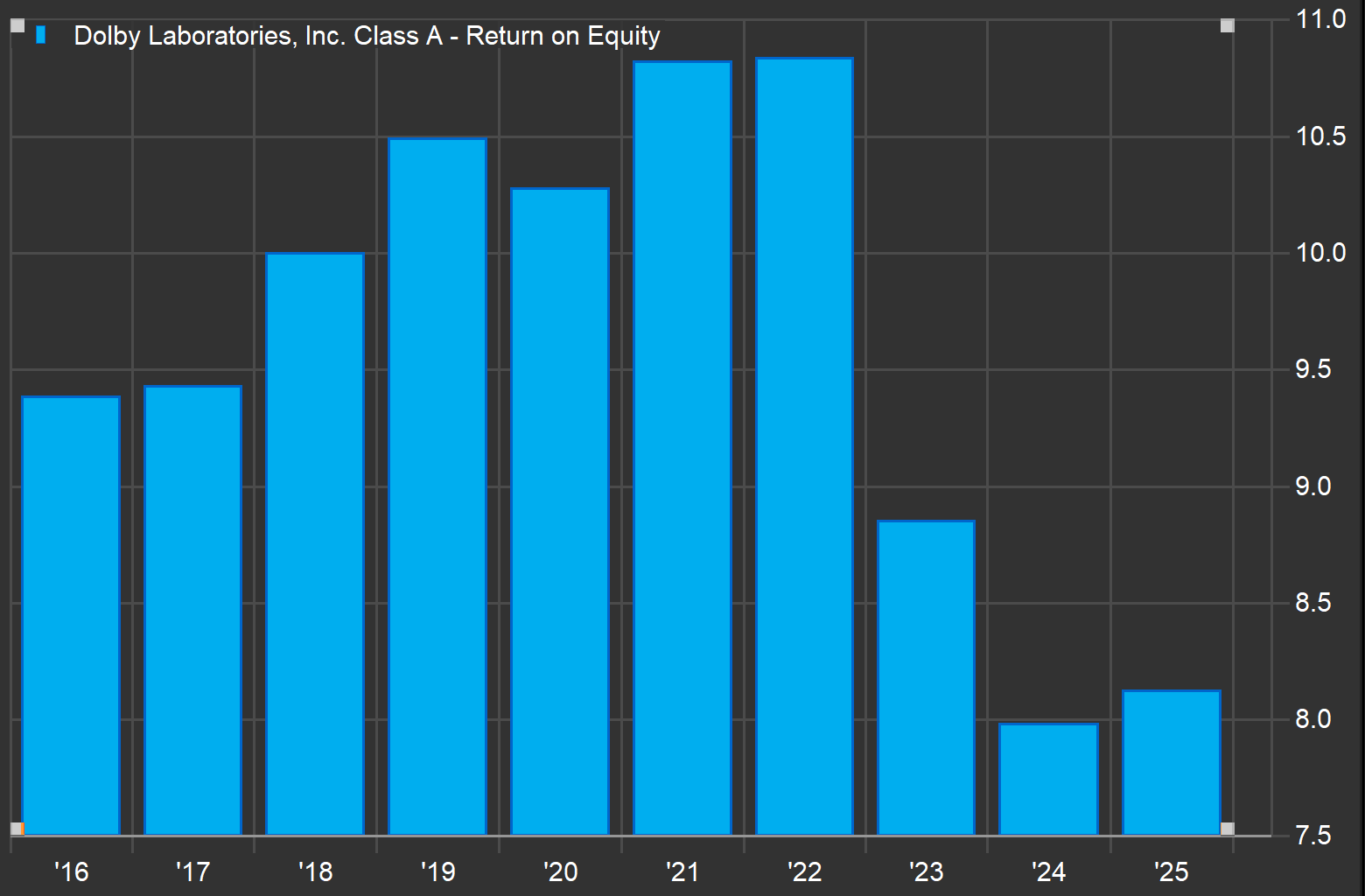

But, for a patent base that genuinely expires, the amortization is a real economic cost, so non-GAAP measures of cash flow overstate true earning power. Dolby spent $429M plus ~$262M/year of R&D and produced flat revenue. Much of Dolby’s "growth" spend merely replaces expiring DD+/AAC/AVC royalties. If replacement capital earns only its ~8.7% cost of capital, the spending is value-neutral despite sustaining reported earnings. Dolby’s return on equity has indeed fallen towards its cost of capital.

Disclaimers, and then some

Aside from the standard disclaimers below, yes, I am short Dolby. Between the dividend and the cost of borrow this costs me approximately 3.25% annually. I expect Dolby’s share price to slowly converge to the present value of only its steady state earnings power over the next 5 years.

That would be a decline of ~15% annually, a targeted 11.75% annualized return on my short. That said, I don’t really care if Dolby declines further or not, I just don’t want it to go up. I am happy to have low-cost financing for my longs. I am generally attracted to royalty companies, and one of the reasons I have such confidence in this short is that I began my research looking for a bull case for the stock. I found none.

Of course, these days a well-worded press release around an AI pivot can cause hyperbolic reversals of a company’s share price. I find that risk somewhat tempered by the comfortable financial and governance position of the Dolby family. My sense is that they are happy with company’s ability to generate mailbox money for at least the next decade even if the core business is slowly melting.

The Dolbys’ largesse is my gain.

This report is intended to be educational and entertaining, not investment advice. Do your own due diligence. I make no representation, warranty, or undertaking, express or implied, as to the accuracy, reliability, completeness, or reasonableness of the information contained in this report.

Any assumptions, opinions, and estimates expressed in this report constitute my judgment as of the date thereof and are subject to change without notice. Any projections contained in the report are based on a number of assumptions as to market conditions. There is no guarantee that projected outcomes will be achieved. Lewis Enterprises is not acting as your financial advisor or in any fiduciary capacity.