Harvard's Water

The Challenge of Long-Term Institutional Investing

One hundred and twenty thousand acres of nuts and fruits and berries in California and still counting. They had survived the drought. Did it teach him any lessons?

“Lessons?” he says, sounding perplexed. “Who knows when a five-year drought is coming? Who anticipates that you can’t fill a water bank for six or seven years?”

“Come on,” I say. “It’s California.”

“Sure. But you take some risks in business. And when you’ve been as lucky as we’ve been, you start to think you can ride out drought, too.”

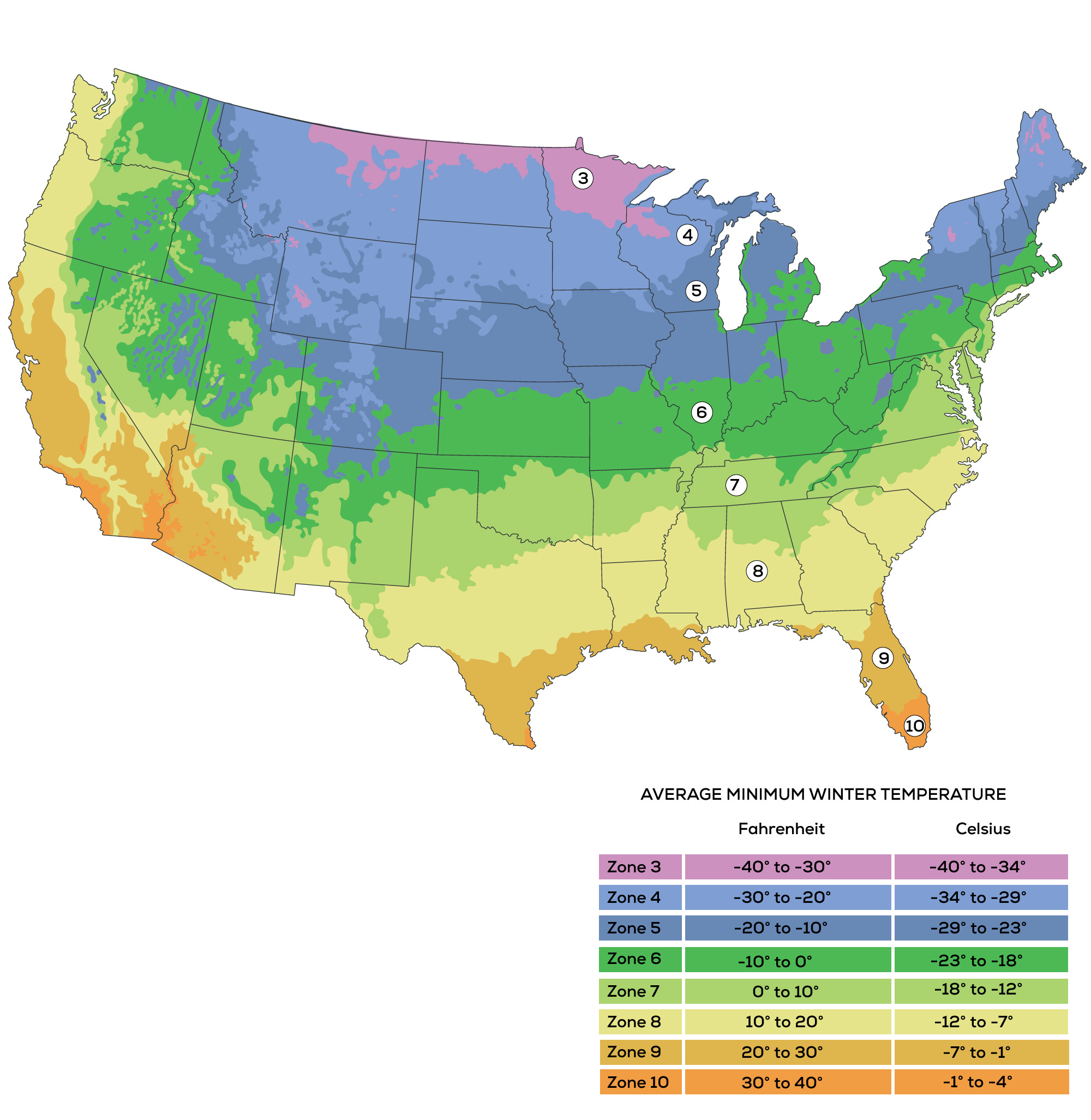

Longer time horizons are one of the few edges left in investing. Being able to express a through-cycle-and-beyond thesis can open up an entirely new world of opportunities. Several years ago, I attended an agricultural investing conference. One of the groups was pitching a strategy that purchased orchard lands just above the ideal USDA zones. The USDA publishes “plant hardiness zones” that indicate the best geographies for certain crops based on weather patterns. For fruit and other tree crops Zones 5 and 6 are ideal, but this group believed that climate change would push those zones to the north. They could buy orchard lands for cheaper outside of the ideal zones.

While tree crops already face a significant “ J curve” before producing any cash flow, these investors were thinking in geological time frames. They may be right, but finding capital partners willing to commit to such a strategy is challenging. Most LPs want to be serious, long-term investors but they aren’t interested in “getting married”. In reality, they need to rebalance, be tactical, responsive to boards and other, mostly bureaucratic, features of institutional capital allocation.

Endowments are unique in some sense because their capital is intended to last into perpetuity. Well-funded universities often have modest withdrawal rates from their investment holdings which allows the managers of these funds to take unique risks with their capital. As David Swensen brilliantly identified, the core element of great investment returns for endowments is establishing “uninstitutional behavior” from within an institution. Swensen:

Establishing and maintaining an unconventional investment profile requires acceptance of uncomfortably idiosyncratic portfolios, which frequently appear downright imprudent in the eyes of conventional wisdom. Unless institutions maintain contrarian positions through difficult times, the resulting damage of buying high and selling low imposes severe financial and reputational costs on the institution.

This key precept is often overlooked in the structure of investment policies, investment teams, and governance bodies. Investment themes often outlive their agents and stakeholders. Without robust policies to combat institutional behavior, well-considered investments can be derailed by a host of fallacies that plague consensus-driven investment organizations.

The Endowment Approach

Starting shortly after the GFC, using opaque LLCs and local operators, Harvard began amassing large tracts of marginal agricultural land in California at well above market prices. Both the buyer and the prices they were willing to pay were baffling to the locals. Of course, Harvard wasn’t interested in the provincial business of farming or winemaking, they are natural resource investors, and they were purchasing land that sat atop aquifers. From the Wall Street Journal:

With the land, it was acquiring rights to vast sources of water in a region where the earth’s warming is making the resource an ever-more-valuable asset. Drought has plagued California in recent years, hitting farmers particularly hard. The Central Coast experienced drought conditions for 30% of the past two decades, compared with 14% of the prior 100 years, a 2015 study found…The $39 billion fund, among America’s biggest endowments, now values its vineyards at $305 million, up nearly threefold from 2013, while its overall natural-resource investments have done poorly.

This is a strategy Harvard deployed across the globe, making a long-term bet on “The World’s Most Valuable Resource.” According to GRAIN, Harvest assembled some 800,000 hectares of Farmland:

Harvard's endowment fund has spent around $1 billion to acquire control of an estimated 850,000 hectares of farmland around the world, making the University one of the world's largest and most geographically diverse farmland investors.

This is no easy task in real estate. Being a large buyer in illiquid markets can be deleterious to returns as sellers begin to see and understand your true thesis and set their own pricing to capture a portion of your prospective economics. Harvard used a variety of byzantine structures to conceal the size and scope of their portfolio. In Brazil, where foreign ownership of land is partially restricted, Harvard used local operators and companies to conceal and amass their holding. In fantastically colorful wording a Brazilian panel found that Harvard used a “festival of irregular and illegal procedures which resulted in usurpation of public lands.”

In California, where the allocation of water resources is administered through an intense political and bureaucratic process, Harvard sought to increase the value of their holdings through political action. Cindy Steinbeck (yes, Steinbeck) a grape grower in California wrote,

The local perception, right or wrong, is that Harvard has been doing the following: making purchases using multiple layers of disregarded entities such that it would be difficult for the layperson to trace the purchase back to Harvard; using agents to push for formation of a local water district that would allow Harvard’s properties to ultimately benefit from government grants and taxpayer funds; inducing certain property owners to sell with offers that are many times the going market rates and using this method to acquire properties that contain public water infrastructure; and generally not being forthcoming with the local populace about how these investments could affect the most vital of resources—all in the name of returns on investment.

The World’s Richest Farmer

Like the wheat barons of the 1870s who lived on San Francisco’s Nob Hill, Resnick isn’t of this place. He’s never driven a tractor or opened an irrigation valve. He’s never put a dusty boot on the neck of a shovel and dug down into the soil. He wouldn’t know one of his Valencia orange groves from one of his Washington navel orange groves. The land to him isn’t real. It’s an economy of scale on a scale no one’s ever tried here.

In California Sunday Magazine’s A Kingdom From Dust and subsequently in the book The Dreamt Land, Mark Arax beautifully tells the story of Kern County, its land, its water, and its largest user, Stewart Resnick. Resnick, in addition to brands like POM Wonderful and Fiji Water, controls over 60% of the US pistachio crop as well as significant holdings of almond and mandarin orchards through the privately held Wonderful Company.

Keep reading with a 7-day free trial

Subscribe to Lewis Enterprises to keep reading this post and get 7 days of free access to the full post archives.