L.E. Guest Post | The Great Taiwan Bubble

Fear, FOMO & Greed in an Emerging Market

There is less value in naming a precise turning point than recognizing the requirement of making many successive difficult decisions that far exceed the human mind’s capacity to do so without error

If you have confidently navigated public markets over the past three years you can stop reading. For the remaining mortals, the recent market regime has offered no shortage of “What the hell is going on?” moments. I have returned again and again to this piece about the Taiwanese stock bubble of the late 1980s by The Magic Bakery this past year. Drawn largely from the book The Great Taiwan Bubble by Steve Champion, The Magic Bakery highlights the parallels that we saw during the 2020-2021 market run-up. As we enter a new period of potentially mimetic valuations ( NVDA 0.00%↑ currently trades at >180x earnings) it is worth recalling the underlying themes of the Taiwanese bubble: Subsidized trading, novel market structures and specious disclosure.

The Magic Bakery brilliantly extends this review to the psychological toll it takes on investors. “Sorosian” notions of profiting from bubble dynamics belies the challenge of compound decision-making in a fundamentally irrational environment. Enjoy and subscribe to Cheap Thrill Stocks.

The Great Taiwan Bubble by Steven Champion

Capitalism With Chinese Characteristics

“When I see a bubble, I rush in to buy it.” – George Soros

“Just tell me where I’m going to die so I don’t go there.” – Charlie Munger

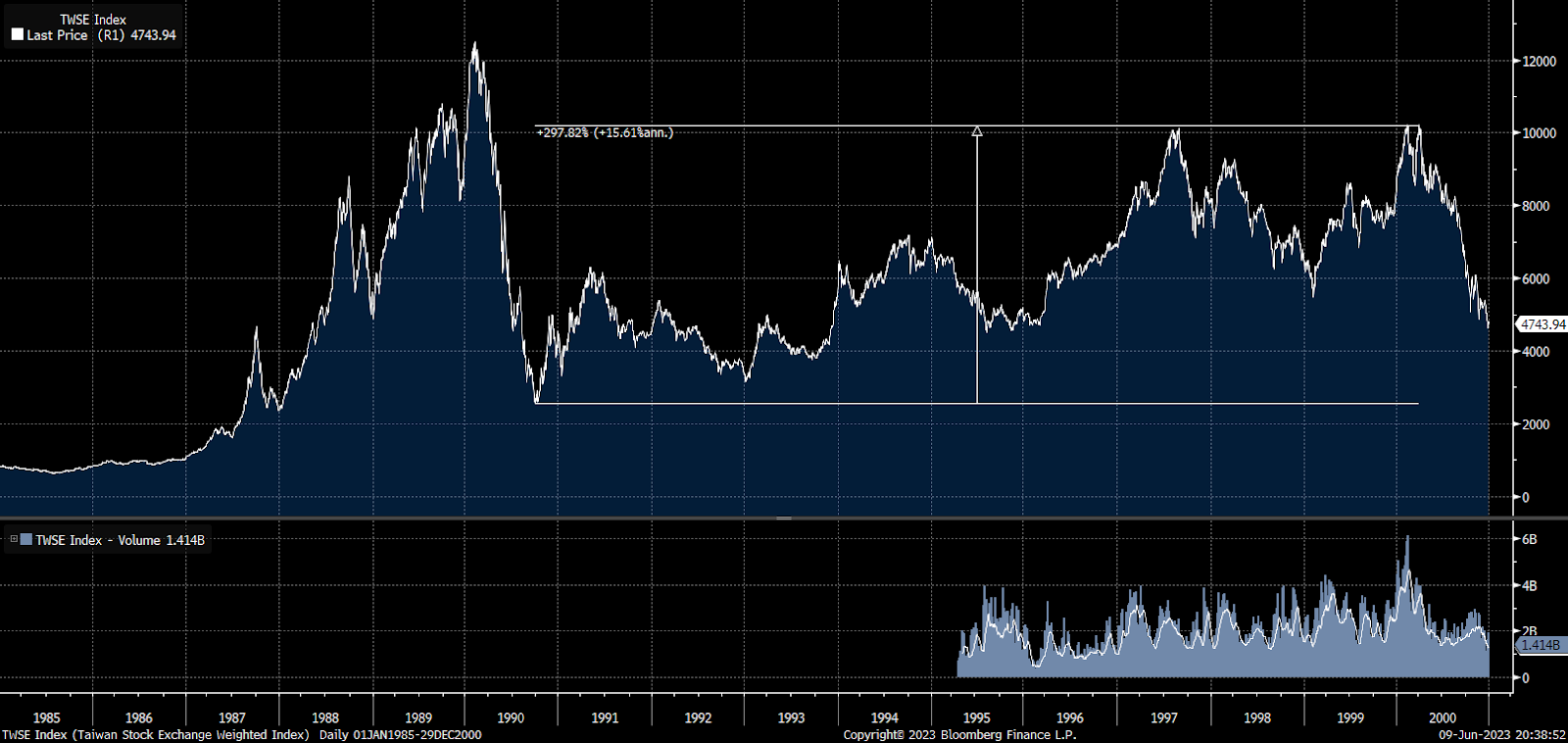

The Taiwan Stock Exchange Index went up over 1,200% over three years in the late 1980s. For comparison, the S&P is only up 660% from its March 2009 low thirteen years ago. This period presents one of the more illuminating case studies on bubbles despite it being mostly relegated to a dark corner of financial history. The stock market in 2020 and 2021 highlights the importance of understanding past analogs. Steve Champion’s The Great Taiwan Bubble recounting of this period is based on the author’s participation as a Taiwan-based, Mandarin-speaking manager of a Taiwan-focused investment fund during this period.

Backdrop

This bubble is not distinct in the annals of financial history at first blush. There was an accumulation of savings in an export driven high growth economy which generated excess liquidity. Taiwan went from very little in the way of international reserves in the 1970s to $20bn in 1985 and then $80bn by 1987 with the currency appreciating 60% from 1985-90. GDP growth was in the 6-8% range with building enthusiasm for Taiwan’s increasing access to the mainland Chinese market. It should not be surprising that optimism drove sentiment past some calm equilibrium.

Where the Taiwan bubble really stands out is its relative scale. Despite being overshadowed by its successors in the Asian Financial Crisis, the magnitude of the Taiwan bubble far exceeded what was seen in the runup to the AFC. The P/E multiple for the stock markets of Indonesia, Thailand, and Malaysia were 22, 26, and 28, respectively, at their peaks. The P/E multiple in Taiwan reached 100x near its peak in the fall of 1989. Taiwan’s bubble lacked the large current account deficits, debt fueled malinvestment, or foreign casino capitalist locusts in either the run up or the aftermath compared to its Asian Tiger peers. The extremity of valuation combined with the inability to dismiss it as stemming from bad exogenous behavior makes this case applicable to the present.

It’s the market structure, stupid

The valuable lessons from Taiwan Bubble reside in the market structure and the players.

Low transaction costs were standard in Taiwan in the 1980s, which enabled trading hyperactivity across a broad cross-section of the population that parallels 2020 and 2021. Commissions were fixed at 0.15% as computerized trading was introduced in January 1987. The average daily volume on the Taiwan Stock Exchange was equal to that of Tokyo, Frankfurt, and New York by early 1990. The share turnover (value of traded securities relative to total market cap) for the entire market increased from 200%, already quite short, to 600% from 1986 to 1989. There were 4.6m active brokerage accounts by 1990 in a nation of 20m people, so essentially everyone was trading a lot. For context, in the US today there are about 100m brokerage accounts in a country of 330m.

The number of brokerages mushroomed over this period from 27 to 297 from June 1988 to March 1990, facilitating and profiting from this large trading activity. The pre-tax profits of TSE brokerages increased from $110m to $1,174m from 1986-89. This parallels the rise of Robinhood’s zero-cost trading and the attendant profitability of Virtu or Citadel. There is an underlying business model that requires a large amount of volume; either from scale in near zero commissions or scale in consolidating order flow to sell to offset zero commissions.

Trading activity was guided to areas prone to manipulation. “Full delivery” companies, which are the equivalent of shell companies, were a highly active corner of the market. These companies had no income, assets, or employees, but remained listed. Specific market structures beyond low commissions enabled sharp price movements. There were price limits on daily changes which created self-fulfilling share price swings. The trade backlog was visible even after the daily price movement had resulted in a halt to trading. Someone could place a large order without the need to execute it, which would spur others to place orders as well. While not as explicit as “payment for order flow” today, the order flow itself became an important market data point and large profit pool for certain market players.

One documented manipulation was in a closed-end fund called Citizens Fund. A pumper advertised job openings for officers at the fund in exchange for handing over control of a certain number of shares. Investors obliged. This cornered the supply of shares in the market as they were effectively taken out of the free float. The price of Citizens Fund moved from a 28% discount to its net asset value (NAV) to a 227% premium of NAV. The “officers” of the company were unable to sell into the illogical pricing, but the organizers of the scheme could after the tight float drove up the share price.

Gamma squeezes in highly shorted companies best demonstrated by Gamestop in January 2021 are a similar metagame that takes profits from market structure and hyperactivity. DeepFuckingValue did articulate a case for Gamestop prior to its January 2021 squeeze that made note of the short interest combined with hope the death of the underlying business was overstated. There were professional investors who profited from Gamestop as well, although some may admit more chance than foresight. There were even more complicated maneuvers some professionals undertook to profit from the temporary structural dynamics in AMC.

The men and women merely players

Numerous speculators gained attention as major players in the market - Grasshead Tsai, Exorcist Yu, Little Boss Weng, King of the Monster Bulls Cheng, Antique Chang, Chili Pepper Chiu, Little Devil Tsai, Big Tuna Chuang. Their market calls were followed by retail investors. Players with big followings would simply release a price target on a stock that would then become a reference point for retail players. Stock “fan clubs” placed daily coded advertisements in the financial pages to advise clients of rapidly changing phone numbers that they could call for a stock tip of the day.

None of this is a far cry from the retail investor behavior seen in 2020 and 2021. The medium is barely tweaked and the message remains the same from r/wallstreetbets or Discord trading groups (Discord trading, r/wallstreetbets trading). Chamath Palihapitiya puts out one-page memos for his SPAC investments (Metromile, Clover, Proterra). One of the noteworthy drivers behind the price movements in SPACs is a combination of harnessing retail trader interest in zero cost trading fueled meta games like gamma squeezes, more sophisticated players’ knowledge of these metagames, and the low float dynamics created through lockups.

Twilight Zones

There were two ways to become a certified public accountant in Taiwan. The first way was to pass an exam, which had such high standards that the pass rate was 1-2%. The second way was as a political reward for long tenure as a teacher or soldier. Pricing for services was competitive because there was a pool of service providers who had no reason to care about checking bank account balances or the age of inventory. Financial statements were stamped with the personal seal of an individual CPA, not the name of a firm. So the opinion letter of the auditor in financial statements would appear to be official in some sense, but the numbers are only as good as those who report and validate them.

The norms of the legal system were distinct from the baseline Western perspective. Enforcement of a law often depended more on relationships than facts or circumstances, according to Champion. Champion gives the example of an unnamed “near bank” in Taiwan controlled by a wealthy and politically connected family. An American financial institution purchased a minority stake in the entity.

While the Taiwanese company was not legally a bank and could not legally accept demand deposits, they did essentially accept demand deposits. Technically speaking the demand deposits were shares in investment portfolios with a fixed term and a variable expected return, but they could also be withdrawn at any time at a minimum guaranteed yield. American auditors were uncomfortable with this. The American shareholder sought to clarify matters with the Taiwanese management. Even with the discomfort of the American auditors, the Taiwanese auditors qualified the financial statements. Regulators had even fined the company a token amount for the transgression. This behavior continued because the near-bank still earned far more as a result of these “deposits” than any fines they had to pay. In discussions with the US company, the president of the Taiwan company referred to the numerous pictures in his office of him alongside major American and Chinese business and political leaders to demonstrate any issue could be resolved through connections. While this specific company did successfully continue to increase its legitimacy without issue, according to Champion, it does demonstrate how vague the legal and accounting frameworks can be at times.

There are plenty of similar ontological quagmires when it comes to accounting or law in US markets today. Bill Hwang and the use of single-family office exemptions to elude margin restrictions by using multiple prime brokers shows the murky nature of the legal system even in the US. Considering that he settled an insider trading investigation in 2012 without admitting or denying wrongdoing, his prior experience likely did support his flexible interpretation of the law. Coinbase is in the early stages of its legal and regulatory journey, which has the implication of making some of its practices still open to interpretations. The US and China are at odds over what they are willing to accept as an auditor on financial statements.

Notes from the underground

Underground financial products, which exist in parallel with regulated financial institutions, were prevalent in Taiwan. It was common for them to offer 4-10% monthly returns. The government-controlled press would print underground exchange and lending rates. The data was included in monetary statistics put out by the Central Bank. It was common to use official bank borrowings at a lower rate to invest in the higher rates offered by underground banks.

Homey Group was an underground bank that at its peak would have been a top 50 bank in the US ranked by deposits. There were approximately 200,000 depositors with peak deposits of $7.4bn. Homey’s Chairman had been prosecuted for robbery, fraud, possession of stolen goods, assault, and forgery when he was younger. He purchased the Taiwan affiliate of a Japanese company that collapsed after a financial scam where pensioners were sold nonexistent gold bars. In exchange for converting the gold bar claims into deposits in a new company, Homey, the pensioners maintained their principal and earned 4%/month on it. Homey invested the funds in speculative stocks, a department store, a movie studio, a hotel, an ad agency, a basketball team, foreign exchange, and lots of real estate in the hopes of sustaining a high monthly payout. In the later stages of this scheme, depositors agreed to extend their deposits for a year, but in doing so switched their securities into a Hong Kong affiliate where they gave up their right to receive a return of principal and instead receive dividends instead of a fixed interest rate. Before eventually declaring bankruptcy in May 1991 with $3.6bn of deposits and 160,000 depositors, the Ministry of Finance had said what it could do under its legal charter and had referred Homey to the Bureau of Investigation seven times, who said Homey was the responsibility of the Ministry of Economic Affairs, who then referred the matter back to the Bureau of Investigations.

The background of Homey group is a good case study on how warning signs get ignored in favor of greed and hope. There are seemingly novel securities in the US that exist in a legally immature state in the form of cryptocurrencies and their adjacent products, such as staking. Their existence is not a secret and the fastest government response came from the IRS to secure tax receipts. Tether, a stablecoin, which would rank as a top 50 bank by deposits today, already seems to be a potential repetition of the Homey saga, from colorful personalities to hard-to-trace funds.

In November 2021, the total value of locked-in decentralized finance projects hit $250bn. That is enough to be the 12th largest bank in the US by deposits, between Charles Schwab and State Street. Much of this appears to be in “yield farming” products that offer anywhere from 4% to 50% or higher. You can find articles referring to instances where depositors have found out someone else walked away with their money or the nebulous nature of their regulatory standing. Despite aesthetic differences, the internal mechanics of opaque financial products and their alluring headline yields appear quite similar across time.

Playing the game

My observations of the present and reading of the past are inconclusive when thinking of how exactly to act when presented with these circumstances. While there is the Sorosian desire to somehow profit from trading such a bubble, the magnitude of the swings between the bottom and the top present formidable psychological obstacles to doing so. At the individual stock level, those that had the highest price increases defy any notion of rational foresight that would be necessary to purchase them.

Even with the full knowledge of hindsight, it is hard to conclude that adeptly investing in bubbles is easy. From a summer peak in 1987 of 4,673, the Taiwanese market saw a drawdown of 50% by the end of the year in concert with global markets. You may have earned 42% from the summer of 1988 to the peak in February 1990, but not before a 43% drawdown at the end of 1988 triggered by an increase in the capital gains tax. It was just as dangerous to be long the market as it was to short it. There is less value in naming a precise turning point than recognizing the requirement of making many successive difficult decisions that far exceed the human mind’s capacity to do so without error.

The “rush in” rational irrationality described by Soros seems quaint in the face of irrational irrationality that occurred. The experience of Stanley Druckenmiller in the dotcom bubble shows the folly in trying to play this specific game in the dotcom bubble:

So like around March I could feel it coming. I just — I had to play. I couldn’t help myself. And three times the same week I pick up a — don’t do it. Don’t do it. Anyway, I pick up the phone finally. I think I missed the top by an hour. I bought $6 billion worth of tech stocks, and in six weeks I had left Soros and I had lost $3 billion in that one play. You asked me what I learned. I didn’t learn anything. I already knew that I wasn’t supposed to do that. I was just an emotional basket case and couldn’t help myself. So, maybe I learned not to do it again, but I already knew that.

The value of these historical episodes is as much emphasizing what not to do as it is it to give you a deeper context for not doing it. This allows you to escape the myopia of your personal tilt stemming from an incapacity to time travel beyond any current psychological moment of financial markets. Simply stacking a Druck parable on top of a perceived market peak doesn’t offer more than an amusing quote to bring up when crafting a narrative justification for your own actions.

The more underrated causes, or at least mechanisms, appear to reside in the market structure and the behavior of players that is not covered in any classrooms or textbooks. While you didn’t have to play the metagame of gamma squeezes in AMC or Gamestop, a player of the more pedestrian long or short equity game should still have been aware of what metagames may be played with their games. There is less explicit literature on this because its main value is to practitioners and the activity itself is an inherent blind spot of academics, but history does offer numerous episodes for further study if you are willing to seek them out.

Further

The Great Taiwan Bubble: The Rise and Fall of an Emerging Stock Market by Steven R. Champion

Michael Fritzell of Asian Century Stocks wrote another fantastic historical account of the Taiwanese bubble.

As a brief epilogue, the Taiwanese Bubble also…wasn’t. From trough-to-peak, the market compounded at 15% annually until the dotcom crash in early 2000.

| A guest post by

|