Summary

As we begin 2025, here are the key REIT themes I'm watching this year. While macro conditions appear increasingly favorable, recent volatility suggests another dynamic year ahead:

Beyond the sector's modest 4.9% return in 2023 lies a remarkable story of divergence, with a 52-point performance gap between subsectors highlighting opportunities for active investors.

Interest rate volatility continues to create compelling entry points, particularly in REITs with strong underlying fundamentals but rate-sensitive trading patterns.

The retail REIT sector exemplifies the danger of compelling narratives obscuring fundamental challenges, despite apparent tailwinds from limited supply.

A historically wide valuation gap between REITs and broader equities, combined with healthy balance sheets, creates an intriguing setup for 2025.

Major 2025 Predictions

Finally, I have not published with nearly as much frequency as I had planned. As a result I am cutting prices on paid subscriptions by more than half. While the experts all agree that frequency and consistency are more important than quality (for sucessful newsletters) — that is simply not a trade I am willing to enter. As always, thanks for reading.

REITs ended the year up 4.9%, collapsing in the final months of the year after returning more than 15% through September. That brings the five-year compounded return, as measured by the FTSE NAREIT All-Equity REIT Index, to 3.28% -- hardly compelling compared to the Nasdaq 100’s 19% run rate over the same period. It is revealing how a bull market can shape expectations. No wonder I get weird looks or, more commonly, silence when I tell people I am a REIT investor.

Pick 4

Market conventions dictate speaking in index terms. However, just as S&P 500 performance refers to a small subset of technology companies, the REIT index-level returns conceal a more opportunity-rich environment. There was a 52% spread between the best and worst-performing sub-sectors.

While some winners, like data centers, align with broad trends and narratives, others, like office REITs, surprised investors. The weakness of post-COVID darling industrial, the worst-performing sub-sector, contrasted with the strength of retail, which outperformed the broader index by nearly 10%. These divergences highlight the opportunity in listed real estate and the potential for active management within the sector.

Buy High, Sell Low (Dividend Yields)

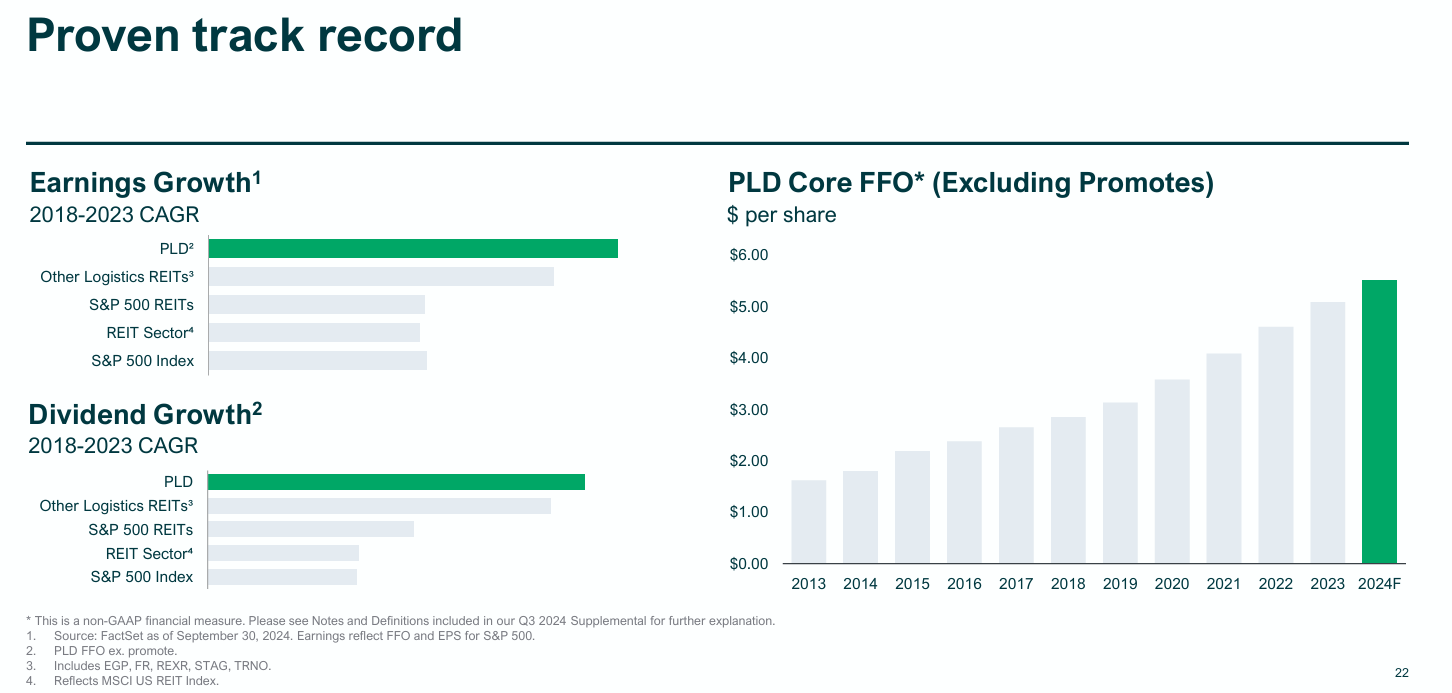

The volatility of REIT equity is far higher than the volatility of underlying property fundamentals. There are few better examples of this than index stalwart Prologis PLD 0.00%↑ . Prologis, the largest publicly traded REIT, represents more than 7% of the index. It is a shockingly consistent performer, growing total revenue and EBITDA by over 13% annually. Yet, the stock has experienced two 25% round-trips this year.

In the modern market, REITs are viewed simplistically as levered exposure to rates and trade as such. Prologis's share price has largely tracked the movements of 20+-year U.S. Treasuries. The company has long-term fixed-rate debt, its leases have embedded mark-to-market gains, and it can largely self-fund growth. Should 50 or 60bps on base rates have this kind of valuation impact?

In December 2023, following PLD’s investor day, I wrote about Prologis's challenging growth prospects and specifically highlighted shareholder return of capital as a potential catalyst.

“I don't believe the stock works unless and until you have a dividend yield greater than 3%. That's a share price under $116 or a 16% increase in the dividend. That dividend increase could come as early as next quarter. PLD has on average, raised the dividend by 12%— today's share price is reflecting it as a near certainty.”

Prologis subsequently raised the dividend, and over the past 12 months, markets have offered investors several opportunities to acquire shares at greater than 3% yields.

With the usual caveats regarding past performance, I looked at 12-month forward returns for PLD shares purchased at yields greater than 3.5% (today’s yield is nearly 3.8%), stripping out overlapping periods. Such a strategy has an 83% win rate and an average return of 36%.

Taking advantage of excess pessimism, passive flows, or misplaced rate anxiety has historically worked well for opportunistic buyers of Prologis. The broader point here is that the entire reason for investing in REITs is exploiting market-driven volatility when valuations come meaningfully detached from property fundamentals.