Dionysius had Damocles seated on a throne and surrounded him with all the luxuries and pleasures of kingship. But there was one catch: a sharp sword hung from the ceiling above Damocles' head by a single thread.

Damocles was initially delighted with his new role, but he soon realized that he could not enjoy the feast or the entertainment because he was constantly afraid that the sword would fall and kill him.

Untold trillions are managed based the foundational assumption that stocks and bonds are negatively correlated. The possibility, the mere suggestion, that this correlation might instead be positive impacts everyone from public pensions to college savers, to the clients of financial planners.

The "prudence" of this assumption is practically codified in law; acting as though it is absolute truth is a matter of fiduciary responsibility. But as Unlimited Funds’ Bob Elliott notes, it is an historical aberration that bonds were such good diversifiers.

The past two years have demonstrated an abject failure of "60/40" portfolios to achieve their stated goal. The obvious objection would be that 24 months is not an adequate time-period over which to judge a portfolio strategy, but that does not make any attempt to explain why asset behavior has changed so much. How could yields rise so dramatically with such little impact on equity valuations?Bill Gross writes in his latest commentary,

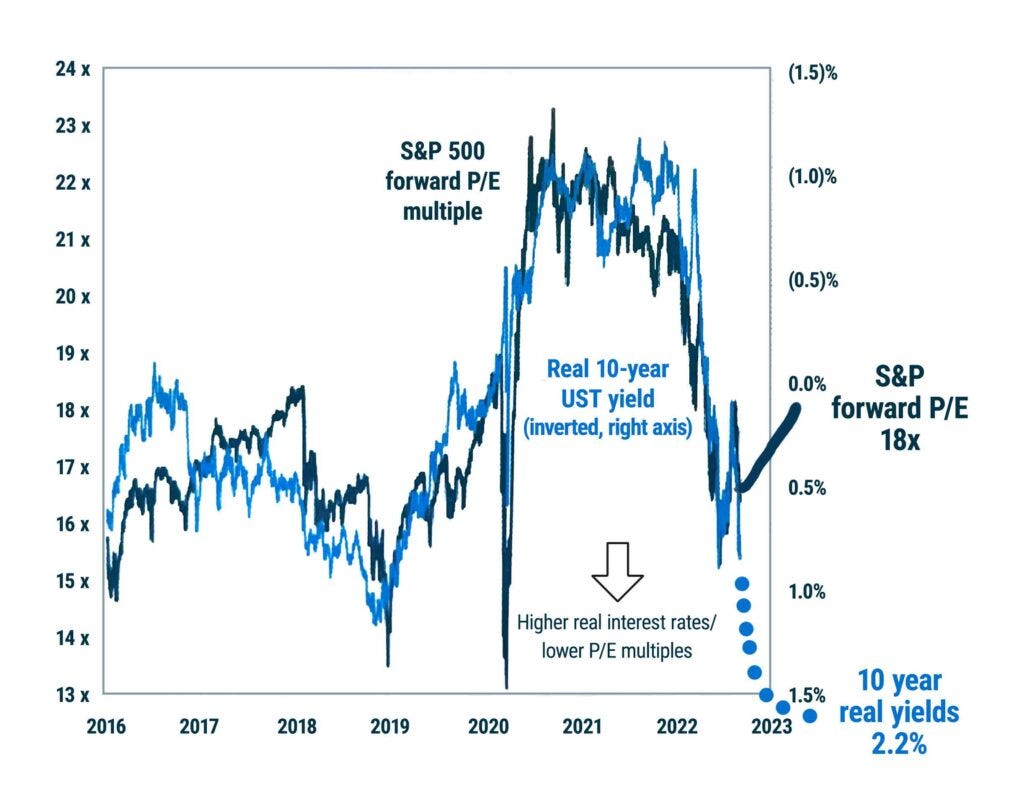

S&P 500 forward P/E multiples have for the last 5 years been correlated to real 10 year Treasury yields with the exception of the last 12 months or so. There is a long-term logic for this. A P/E ratio turned upside down to E/P is really an earnings yield. One might commonsensically assume that if bond yields go up by 350 basis points that (everything else being equal) earnings yields (E/P) should follow somewhat. They did until the Fall of 2022 as the chart will show but not since.

Expressed differently, guaranteeing real purchasing power gains over the next 30 years has become substantially cheaper in the last 18 months. And yet oddly, we see little evidence that this has impacted the valuation of equities.

Gross and Green both identify the thin reeds upon which the equity market may be hanging— the potential for inorganic growth from fiscal spending, an AI-fueled productivity boom, or some secret third thing that powers corporate earnings. All possible, but perhaps pollyannish in the face of rising capital costs and other exogenous shocks.

The biggest issue with this explanation though is the high level of agency it assumes on the part of investors. Let's go back to the original premise: A huge number of assets are managed with essentially no discretion. Target Date Funds, Model Portfolios, and fiduciarily mandated asset allocations are all based on the belief that past is prologue in terms of correlations. Green:

If the dominant mechanism of asset allocation shifts from one where bonds and equities are considered to be substitutes (I can own EITHER bonds or equities based on forward expected return and risk) to one where allocations are FIXED based on the use of historical distributions and correlations, the behavior of asset markets changes markedly.

Extending this dynamic on to a market where the supply of Treasuries is increasing due to monetary tightening and deficit finance, but where many investors are indifferent to yield or relative valuation, creates an obvious distortion.

I find that the elasticity of bond risk premium with respect to supply depends on the correlation between stock and bond returns. An increase in the supply of Treasury bonds raises the required bond risk premiums, but the effect is stronger as stock and bond returns become more positively correlated.

Bond risk premium is a strange beast as it is not directly observable, but conceptually it is the spread investors require for holding long bonds. Hou's paper provides academic backbone for what markets are now experiencing. As bonds lose their utility as a hedge, investors require higher yields to shift their allocations. This creates a reflexive loop for quantitative tightening; higher rates beget higher rates.

But which is it? Are investors not responding to higher yields because they are structurally passive, or are the yields on offer simply not high enough to shift allocations to bonds that no longer offer diversification? What about institutions that are more attuned to the risk exposures of their portfolios?

As Green points out, for asset-liability matchers like insurance companies, higher rates are a boon, reducing their discount factors, but “[p]erversely, this LOWERS demand for bonds even as they become empirically more attractive.”

In a recent interview, Hou refers the inevitability to today's predicament, the specter of recession and subsequent rate cuts as a "Damocles Sword" hanging over the market.

Today a new Damocles Sword hangs over the market: The magic bond yield at which investors will be jarred awake and begin dumping equities to buy fixed income.

Bill Gross,

Unless Chair Powell and company can significantly lower real 10 year Treasury rates from 2.25%, investors may eventually realize that bonds are a better deal than clearly overvalued stocks headed into an economic slowdown/recession.

Those same passive dynamics could begin to work in reverse, or as Mike Green says,

This means that bonds can become incredibly cheap relative to US equities, but the reversal is likely to be quite violent if we see investors eventually challenge these allocation models.

For now, investors are enjoying the feast. When will they look up?