If you know your principles, it's not the decisions that are hard, it's the consequences of your decisions. And I think that that's true for me as an investor. My view is that you figure out what your values and convictions are, and you build your investment strategy around them. And then you know that what's going to be hard is the consequences.

- Dan Rasmussen

From The Intelligent Investor to The Big Short, an image of professional investing has been formed as a truth-seeking pursuit. Asset prices reflect the so-called “wisdom of crowds,” and the fundamental investor frequently considers the crowd wrong enough to be exploited. The job of investing is, through deep diligence, discipline, and research, to be less wrong than the masses, profiting from their short-sightedness and misconceptions.

That thousands upon thousands of intelligent professionals dedicate their lives to this pursuit does not seem to dissuade the fundamental investor from continuing to believe that their view of the future is sufficiently differentiated. They seek opportunities where today’s price is wrong and will correct as time plays out. They believe the future will ultimately align with their vision and line their pockets along the way.

The first threat to this worldview came in the 1960s when academics began studying asset prices as stochastic variables and not solely as reflections of company valuations. Eugene Fama determined that these prices follow a random walk. Later, he and Ken French expanded this work, explaining equity returns as a function of known factors.

Said plainly, all known information was near-instantaneously captured in equity prices. The movement of markets is thus dictated by the parts of the future that are fundamentally unknowable – a terrorist attack on lower Manhattan, a spark that spreads into a raging wildfire, a technological breakthrough from a communist nation.

This view chafes the fundamental investor as it casts their pursuits as futile. However, a larger portion of the investing public found this vision of investing not only true but comforting. That market returns were the best one could hope for eliminated the apparent challenge of identifying investment talent. The rise of low-cost passive investing followed, forming its own sort of religious zealots.

Of course, passive has its own shortcomings. What happens as passive strategies slowly approach 100% market share is unclear. Suppose one considers the “modern” market structure to begin sometime between when Jack Bogle launched the first index fund in 1976 and when Michael Milken was indicted for securities fraud in 1989. In that case, we don’t have much history to judge the efficacy of any investment approach.

Further, piety to indexing forecloses on the quick riches markets seems to have doled out randomly over the past decade. As Charlie Munger famously quipped, “There will always be someone getting wealthier quicker than you...” Today’s investors are left with the choice of chasing alpha and being (statistically) disappointed or ceding the possibility of generating life-changing wealth by adhering to disciplined low-cost indexing.

Dan Rasmussen of Verdad Advisers offers a middle path for investors in his forthcoming The Humble Investor: How to find a winning edge in a surprising world. Rasmussen’s thesis rests on an unassailable truth: The future is hard to predict. But that’s not all; humans’ reluctance to accept this reality is precisely why investment opportunities persist.

Rasmussen relays the experience of Nobel Prize winner Kenneth Arrow, who began his career in the Weather Division of the US Army Air Corps. Arrow noticed that his group, which was responsible for long-range weather forecasts, was underperforming the results using simple historical averages. Arrow submitted his findings to the commanding general, recommending the group be disbanded. When a response finally arrived from the general’s secretary, it read:

“The Commanding General is well aware that the forecasts are no good. However, he needs them for planning purposes.”

An entire financial planning industry is built on this kind of delusion. Rasmussen argues that this misplaced confidence is both the problem and the solution.

Focusing on the much-maligned approach of value investing, the buying of companies trading at low multiples, Rasmussen concedes that the recent past has been unenjoyable. However, over the long run, value wins not because of some natural pull to the mean but because the future's unpredictability ultimately upends the assumptions that drove multiples either up or down in the first place.

Rasmussen quotes Demis Hassabis, CEO of Google’s DeepMind, who argues there are “striking similarities between remembering the past and imagining or simulating the future, including the finding that a common brain network underlies both memory and imagination.” For investors, this expresses itself as a tendency to extrapolate the recent past, positively or negatively. However, Verdad’s own research has found that there is no statistical evidence of the persistence of either revenue or earnings:

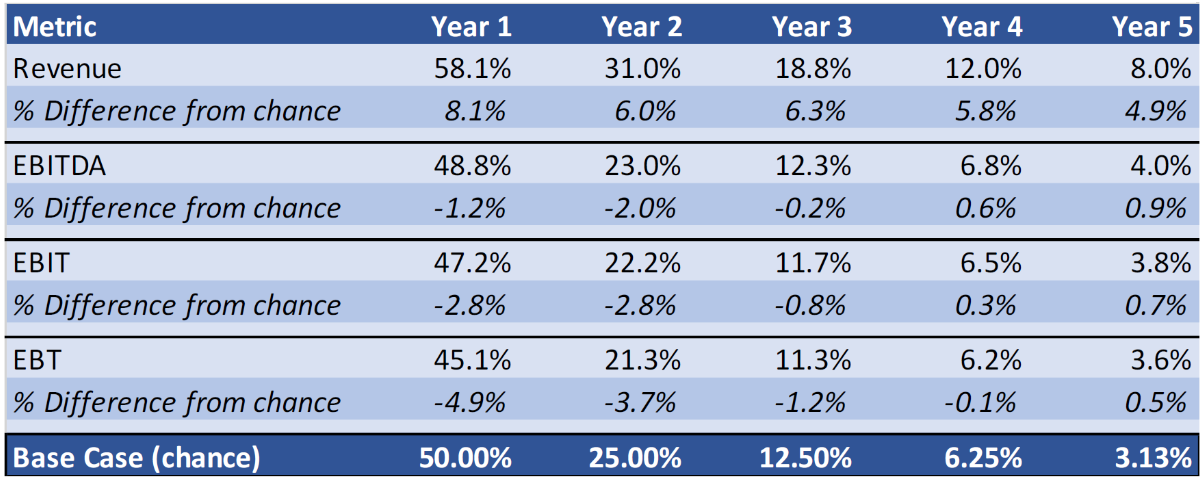

In the table below, we show the proportion of all US companies that sequentially have above-median growth over forward annual periods ranging from one year to five years in a row. For example, within the data, companies that grow above the market median for three years in a row are tagged with a one, and all other companies in the three-year column are tagged with a zero.

The average of that three-year binary column gives us the proportion of companies that outgrow the median each year for three years. This sequential measure of three-year persistence is compared against the probability of randomly flipping the same side of a coin three times in a row (12.5%).

“Sure,” the newly minted Nvidia millionaire may say, “but what about exceptional companies.” Verdad reran the analysis, focusing only on companies in the top quartile. The results improve, but not meaningfully.

Of course, the market is not totally inefficient; some future Nvidias will actually become Nvidia, but mostly they will not. Just as some deep-value companies ultimately fold, many do not, and their fundamental performance improves. In this natural and persistent re-sorting, superior returns can be harvested. Rasmussen,

“The crux of why value investing works is simple. Analyst estimates of future growth are the most important variable in predicting valuation multiples, dominating all other predictors. But growth is neither persistent nor predictable…

…And so, reliably, investors extrapolate past earnings into the future, bidding up the fastest-growing companies and selling down yesterday’s losers, expecting future financials to follow from past financials like eight follows four follows two. And yet, by the time a year or two has passed, the data supported their original thesis has all changed, their forecasts are based on a different set of facts, and what looked like a sure bet then might now have become far less certain, as investor enthusiasm might have moved on from electric vehicles to cryptocurrency to AI.”

Rasmussen takes other “sacred cows” of investing to task with similar quantitative rigor. International investing is dead. It’s not. Private markets are less volatile. They aren’t. Gold and commodities are portfolio diversifiers. Sometimes. Rasmussen tells his readers, in essence, not to trust their lying eyes.

What forms is an approach to investing centered on the belief that the future cannot be predicted and with the humility not to invest based on narratives, no matter how rigorously modeled. Alas, certain beliefs about the future become crowded, and Verdad, to use gambling parlance, “fades” those beliefs.

This works not because theoretical economics suggests that means are reverting or because of some proprietary intrinsic value model. Instead, as the future plays out, the overconfidence of the market gets re-sorted into reality and new outlooks. The strategy relies on maintaining exposure to that re-sorting. That can mean enduring painfully long stretches of euphoria, such as the one we are experiencing now.

“Happy families are all alike; every unhappy family is unhappy in its own way,” wrote Tolstoy. Rasmussen argues that markets are the opposite. Every bull market has different darlings, driven by different trends and narratives, making active investing especially challenging in bull markets. “But crises are alike. Most importantly, we know when we’re in one,” Rasmussen writes. In this way, crises are a bit of a gift to the humble investor.

“Investors who can keep their heads when everyone about them is losing theirs can therefore exploit simple predictable rules to make significantly outsize returns—and have the confidence that the probability of achieving these higher returns is much higher in times of crisis than otherwise.”

Rasmussen quotes a study that found that standard models for predicting equity returns are eight times more predictive during recessions than expansion. Verdad’s research finds that while market returns aren’t much different in crises, factor portfolios perform dramatically better.

📚 A brief factor review... The Fama-French factors are constructed by sorting stocks based on characteristics, then creating long-short portfolios from the top and bottom 20% (quintiles) of stocks.

##

⚖️ Some examples of factors are:

- Market factor (overall market returns)

- Value (HML) "high minus low" High book-to-market vs. low book-to-market stocks

- Investment (CMA) "conservative minus agressive" Conservative asset growth vs. aggressive asset growth

- Size (SMB) "small minus big" Small companies vs. large companies For example, the HML portfolio goes long stocks in the highest book-to-market quintile and shorts those in the lowest quintile.

##

📈 The difference in returns between these quintiles represents the factor premium. The graph shows these factor portfolios significantly outperform the market (25.5%) in both normal and crisis periods, with HML delivering the strongest returns at 79.5% during crises.Crises restore financial propriety. Fundamental precepts about profitability and economic utility that may have been sloughed off during the boom are brought back to the forefront of investors' minds. In the words of mid-century economist John Kenneth Galbraith, “The disenchantment was bound to be as painful as the illusions were beguiling.” Similarly, Rasmussen writes,

“During crises, markets panic, and investor forecasts become too correlated in predicting worse to come. But the humble investor knows that these dire predictions are unlikely to come to pass, as unlikely as the fever dreams that characterize stock manias.”

Today, markets seem to be ascending to unprecedented levels of euphoria. The proverbial Shoe Shine Boy offering stock tips now has a large social media following and a paid Discord. The President and First Lady have launched “official” (unclear what this means in this context) meme coins. If we’re being honest, the exit for Crazytown was actually a few miles back. In such an environment, the thought begins to sneak in, even echoed by famous investors, “Are markets broken?” Rasmussen doesn’t think so,

“I think you just have to remember that part of this is that we live in the US that we're embroiled in this culture, which is simultaneously embracing the S&P 500 and passive index funds and embracing gambling culture. And those things are converging. But we live in a moment of time. And those two phenomenon will not always be the case.”

Staying true to his principles and accepting the consequences, Rasmussen sees our present moment as one where too many people behave with certainty about an uncertain future. Yet across all investment philosophies, humility remains the contrarian trade everyone claims to make, but few actually execute.

The Humble Investor: How to find a winning edge in a surprising world is available for pre-order now and coming out on February 4th.