How to Lose Money

Orange County's Bankruptcy, Bob Citron & DE Shaw on leverage and blowing up

Leverage and power tools share three fundamental properties: they can be extremely helpful, they can allow for greater precision, and they can be really dangerous, even in the hands of experts.

- DE Shaw & Co

Blow-ups have been a feature of financial markets since trade began. Highly levered bets that move irredeemably in the wrong direction or concentrated positions for which the world rearranges a four-sigma event into an inevitability become market legends. The central characters in these episodes are often presented as reckless, feckless speculators that tempted fate for too long or Icarian combinations of genius and hubris. High-profile blow-ups like Long Term Capital Management or Archegos take on a rigidly linearly narrative, their excesses and causes of collapse neatly logical with the benefit of hindsight.

Some truly are forms of financial Russian roulette, “picking up pennies in front of a steamroller” as Lowenstein says in When Genius Failed, but others are the result of complex systems, real-world collisions, and competing moral interests. Financial entropy made manifest. Such is the case with the 1994 bankruptcy of Orange County, California.

Prop 13 and Rise of Bob Citron

The foundation for the Orange County blow-up was laid in June of 1978 with the passage of Proposition 13. Prop 13 stated: “The maximum amount of any ad valorem tax on real property shall not exceed one percent (1%) of the full cash value of such property,” among other measures highly beneficial to property owners. This enormously popular legislation, which led to similar “taxpayer revolt” legislation across the country, had an immediate, dramatic impact on the ability of local municipalities to generate revenue.

The year before Proposition 13 was passed, county governments collected over $3 billion in property tax revenues (34 percent of general county revenues); by 1981-1982, those revenues had dropped to $2.4 billion (22 percent of general county revenues). In response, state aid to counties increased during the same time from $2.09 billion to $3.58 billion, and the state assumed all of the cost of some county programs and part of others. The state also redistributed local property tax revenues. One way in which the state tried to help counties increase revenues was to loosen state restrictions on local government investment practices.1

Enter Bob Citron, a bureaucrat with a decidedly non-high-finance resume that successfully ran for the position of Orange County “tax man” in 1970. In 1973, as a budget-saving measure, Orange County combined the roles of the tax collector and the county treasurer. Overnight Citron, a man who had never owned a single share of stock, became responsible for investing hundreds of millions of dollars of the County’s money for the Orange County Investment Pool (OCIP). Citron’s inexperience caused him to lean heavily on the guidance of Wall Street advisory firms that pushed complex interest rate derivatives and repurchase agreements to fund them. Just as a new generation of traders has swiped their way to high-level options approval on Robinhood, Citron got bit by the leverage bug. By the beginning of 1994, the OCIP had $7.5b of public funds carrying a $20 billion investment portfolio.

Lessons from The Woodshop

Famed quantitative hedge fund D.E. Shaw & Co released Lessons from The Woodshop in their March 2010 Market Insights. It was on the heels of the Great Financial Crisis which was attributed to leveraged trading run amok. D.E. Shaw took a more balanced approach, urging a 360-degree view of leverage.

Put simply, folks think a lot about the question, “How much leverage?” but not very much at all about the questions, “Why is the leverage being used?”, “Under what terms and conditions is the borrowing being done?” and “How is the leverage quantity being computed?

Said differently, both quantity and quality of leverage employed must be considered. This would turn out to be a crucial distinction for Orange County as Citron’s reputation as a money wizard grew and attracted other agencies that weren’t necessarily obliged to invest in the OCIP, but did, drawn to Citron’s impressive track record.

“I don’t know how in the hell he does it,” said Thomas Riley, then chairman of the Board of Supervisors. “But he makes us all look good.”

“How in the hell” Bob Citron was doing it was pretty straightforward: A growing portfolio of levered bets that the yield curve would remain largely unchanged. Citron borrowed at a floating rate and invested at a fixed rate. There were some complex, occasionally exotic, expressions of this strategy, but the underlying bet depended on the persistence of an upward sloping yield curve and declining interest rates.

Citron’s leveraged strategy can be viewed as an interest rate spread strategy on the difference between the four-year fixed investment rate and the floating borrowing rate.

This strategy is akin to an invest floating note, or reverse floater. The underlying bet is that the floating rate will not rise above the investment rate. As long as the borrowing rate remains below the investment rate, the combination of spread and leverage would generate an appreciable return for the investment pool. But if the cost of borrowing rises above the investment rate, the fund would incur a loss that leverage would magnify.

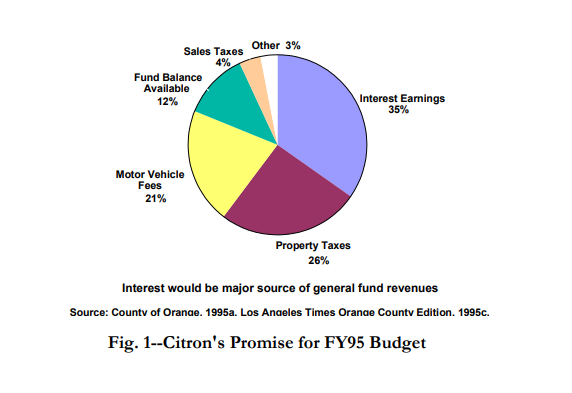

And it was working, at one point earning as much as 10% on equity; a much-needed boon for Orange County where interest earnings were expected to cover well over 20% of the annual budget. However, beginning in 1994 the Federal Reserve under Alan Greenspan started hiking rates aggressively worried about an overheating economy and inflation.

This dramatic move in short-term rates, obviously deleterious to Citron’s strategy, did not go unnoticed by the banks funding him. Citron started receiving regular communication from Michael Stamenson, Merrill Lynch’s Director of Municipal Finance in late 1992 that continued through 1993: